I’m not the most active person on LinkedIn, more of a quiet observer who scrolls now and then. I do make new connections occasionally (selectively, of course). At the risk of upsetting some people, LinkedIn can sometimes feel like a stage where many are more interested in “showing off” than sharing real insights or adding value.

One person I always make a point to follow is Denise Chisholm. Her insights are consistently outstanding, often making me pause, think, and challenge my own views. Here is another timely update from her.

Here is a section:

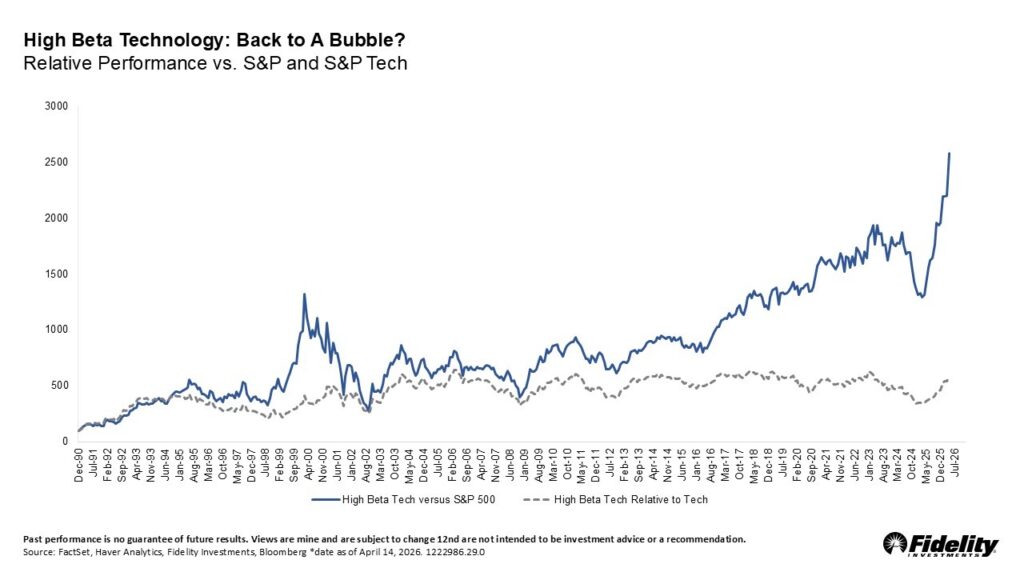

By some definitions, the riskiest technology stocks are up more than 20% over the past three weeks, a move that looks extreme when plotted against the S&P 500. It is tempting to interpret that divergence as a sign of speculative excess (yet again). But the key question is not whether high beta tech has rallied – it is what that rally actually represents.

Is this chart simply picking up the fact that technology remains the market’s leadership group, or are risky tech stocks doing something they do not typically do? History suggests the distinction matters.

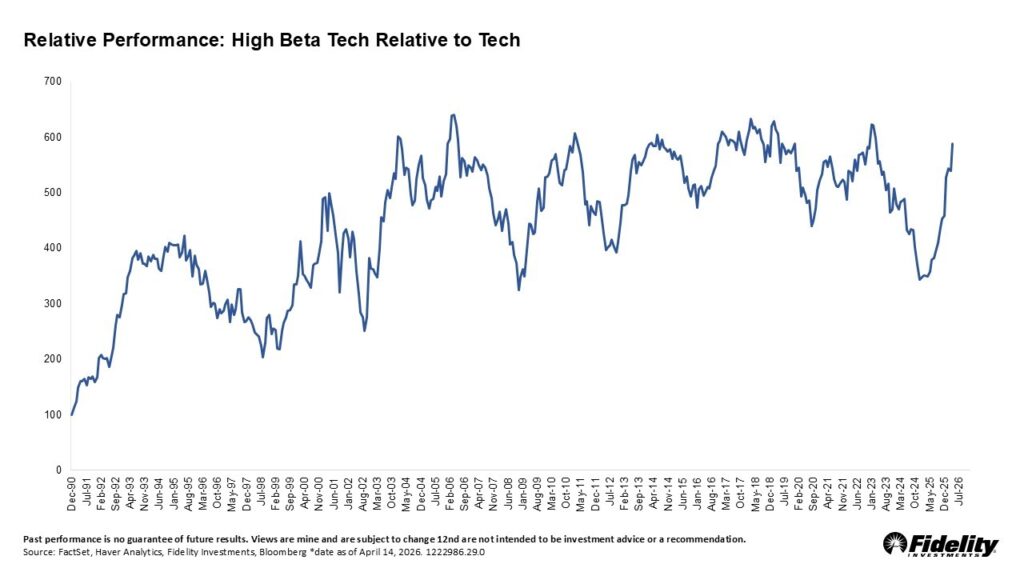

On closer examination, sharp rallies in high beta tech, relative to the rest of the sector, have been a recurring feature of the last two decades. The irony is that despite their eye‑catching bursts, high beta tech stocks have not been the long‑term winners within the sector. Over full cycles, pure risk exposure tends to lag. Point being, taken alone, that chart looks dramatic. In context, it looks a lot like history.

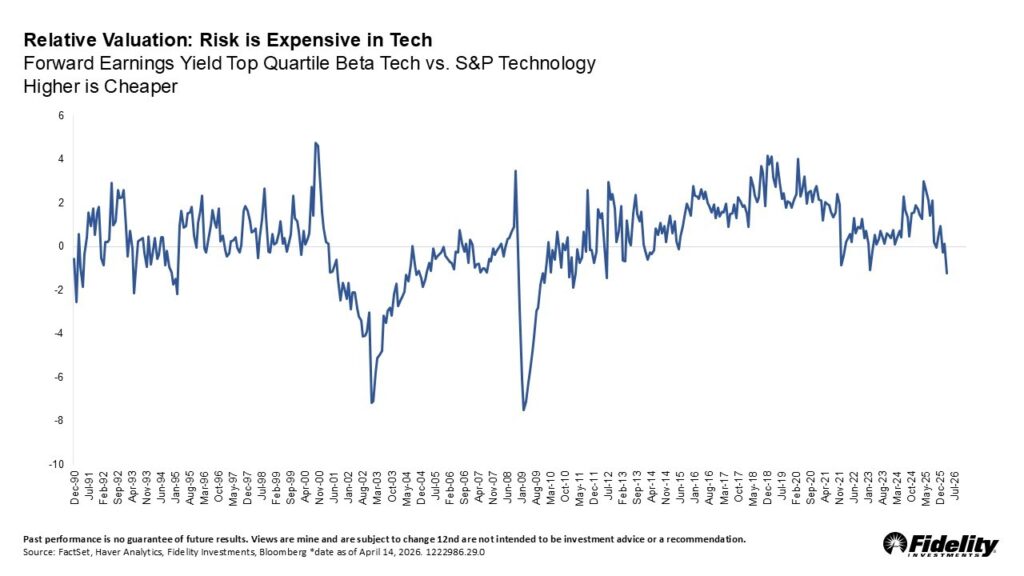

Risky technology stocks are also expensive – and that, too, is a familiar part of the story. It happened most notably during the dot‑com period and the Global Financial Crisis. In those episodes, relative valuations rose largely because earnings were collapsing, not because prices were racing ahead.

That is not what we are seeing today. For the median technology company – much like the median S&P 500 stock – earnings growth appears to be re‑emerging after a period of stagnation. So does expensive “risk” within technology signal that investors should run from the sector? Historically, the answer is no.