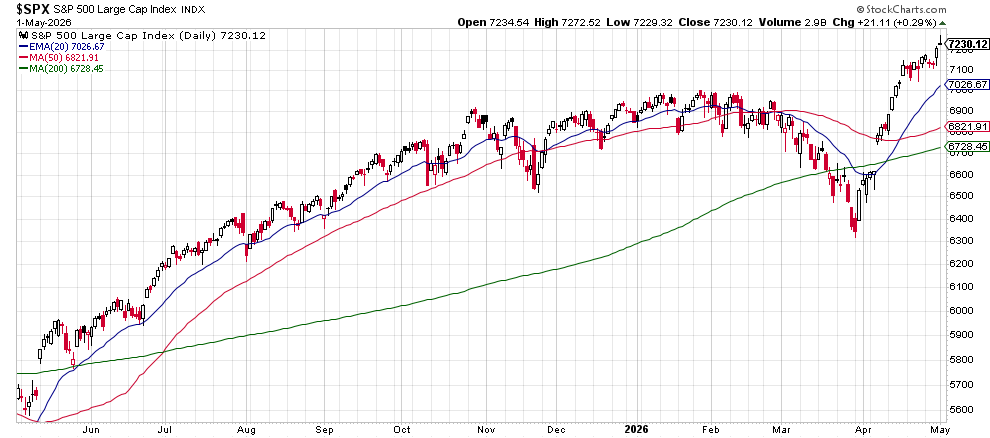

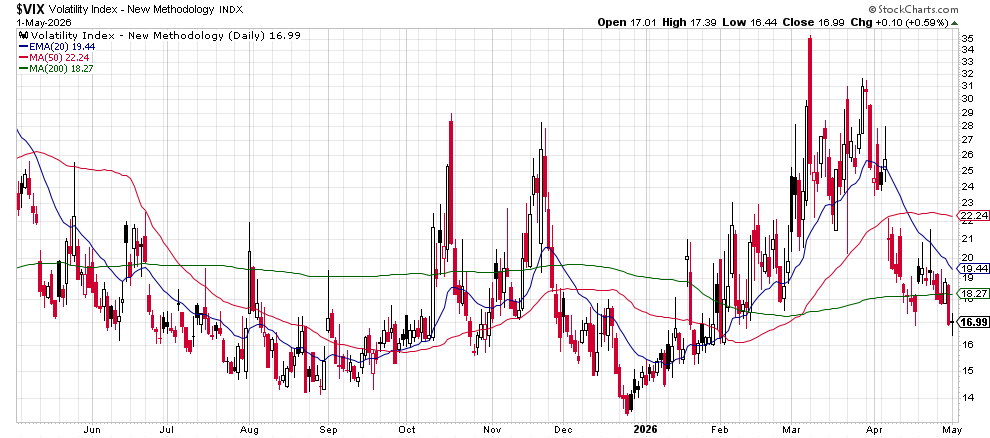

A number of signals in my models are starting to turn, not dramatic, but enough to tell me markets are getting more challenging in the short term. On the surface, things still look fine. Wall Street pushed to new all-time highs in April, helped along by small caps and a solid Q1 earnings season. Yes, April was the best one-month return for the S&P 500 since November 2020. Everyone cheered.

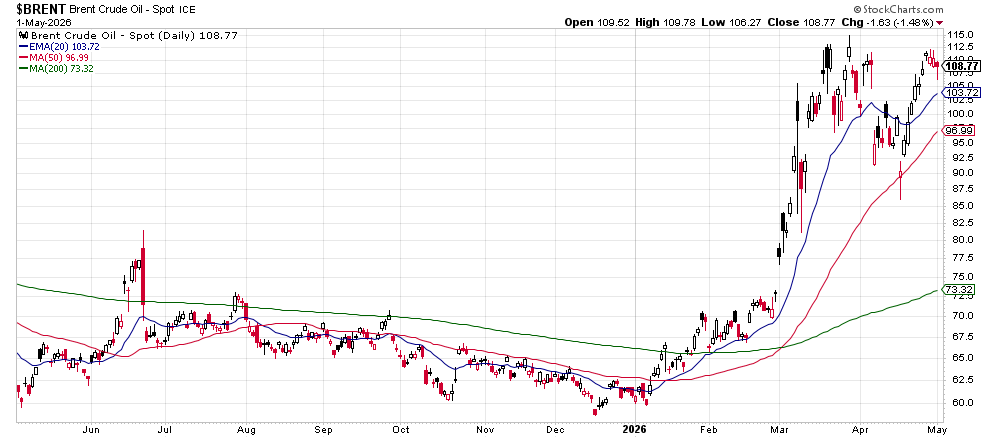

Now we are heading into Q2 with a slightly different backdrop, energy prices are creeping up again and bond yields are pushing higher. Not the kind of combination that makes life easy for markets.

I have been spending more time behind the screens than I would like, making sure we do not get pulled into reacting to every headline that pops up. These are the periods where things looks quiet on the outside, but the real work is being done underneath.

Heading into Q2, I’m turning a bit more cautious on risk assets and adjusting where it makes sense. No need to be heroic here. The job is still the same, protect capital and make sure our more conservative mandates can get through this phase without unnecessary damage. If that also means fewer people waking up at 3am to check prices, even better.

This is also the kind of environment where our alternative strategies are meant to do their work. They are not there to chase upside when everything looks easy, but to manage downside when things get messy so we stay in the game and keep our footing while others are reacting.