I’m not the most active person on LinkedIn. More of a quiet observer who scrolls now and then. One person I always make a point to follow is Denise Chisholm. She does not post about her meals, business class travels, airport lounge reflections, or panel appearances. Well, you know what I mean.

Instead, she posts actual insights. The kind that make me pause, think, and occasionally challenge my own views which is becoming increasingly rare on social media these days.

Here is a section from another timely update from her:

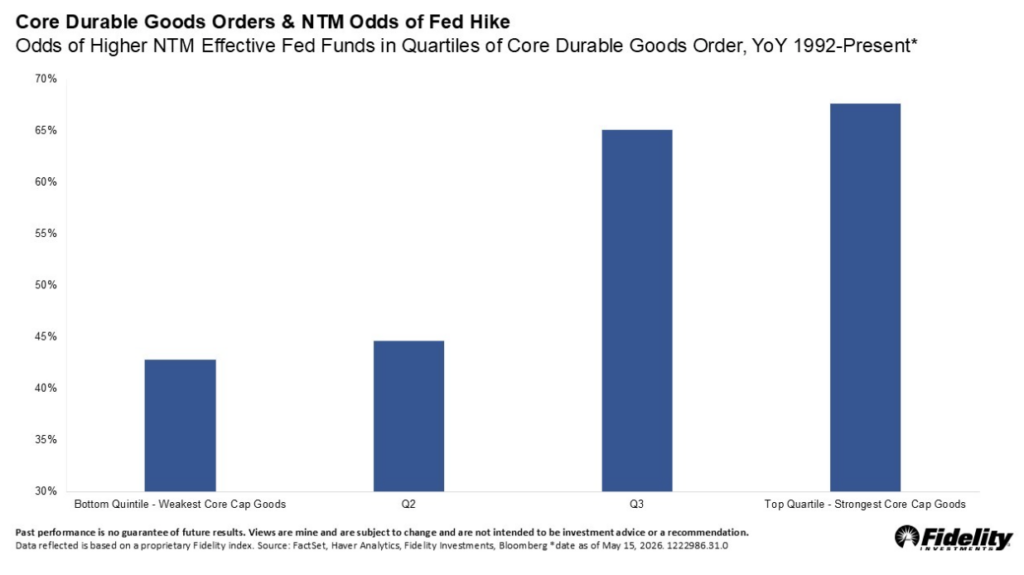

Last week, we highlighted how the increasingly diffuse durable goods data suggests the capex recovery is not only gaining momentum, but broadening, a constructive signal for earnings and, by extension, equities. But buried within that improvement particularly in the top quartile growth readings is a less appreciated implication: stronger growth also raises the odds that the Fed may need to hike.

That may run counter to the current narrative, where many investors see higher oil prices as the factor that is increasing the odds of a Fed hike. But when you examine the data, oil-driven shocks have historically made the Fed less likely to tighten, not more functioning more like a tax on the consumer than a catalyst for broad-based price increases. By contrast, a clearer pattern emerges when it comes to growth: the stronger growth has been, the more likely the Fed is to hike.

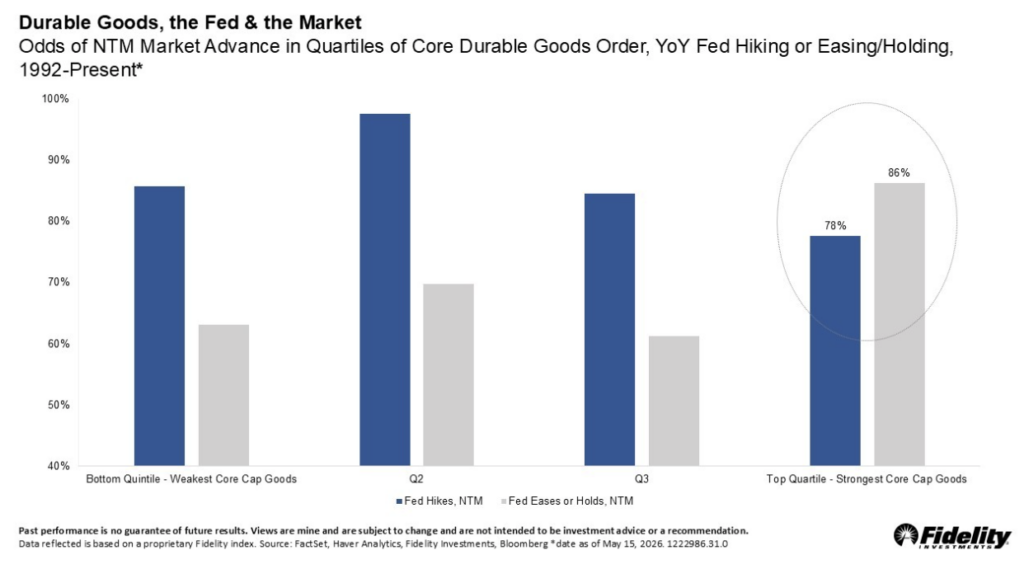

This is where it gets interesting: if growth is the reason for the hike, historically speaking, the equity market has had little problem with it. In fact, when growth whether measured by durable goods (below), GDP, or investment spending is strong, the market has shown above-average probabilities of advancing regardless of whether the Fed is hiking, on hold, or easing.

This gets to an often-misunderstood point: for equity markets, the why behind Fed policy tends to matter more than the direction itself. Rate hikes associated with strengthening growth have historically coincided with favorable equity outcomes not because tighter policy is inherently bullish, but because it reflects a healthy underlying backdrop.

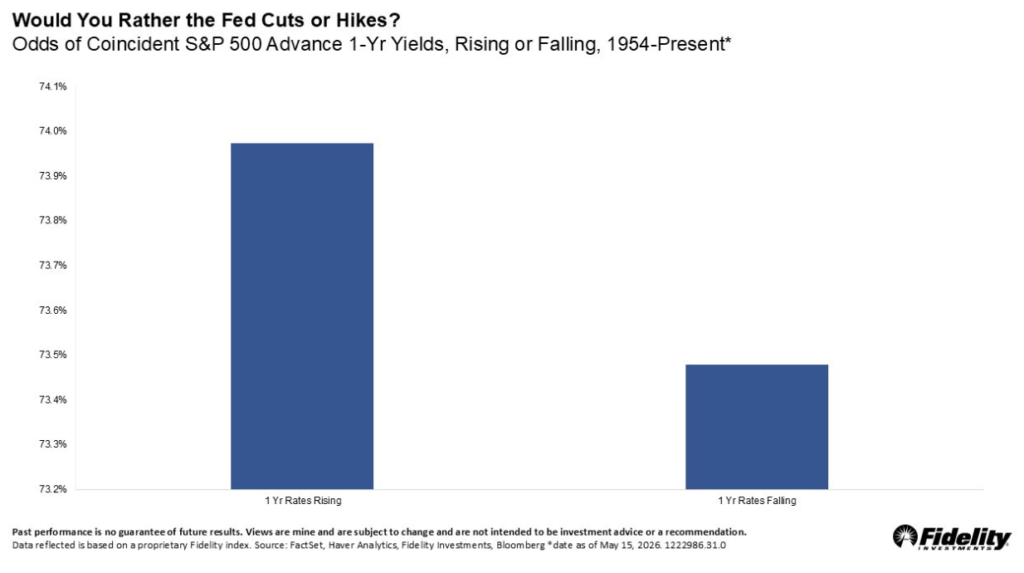

Said differently, the Fed is typically hiking alongside stronger growth and cutting alongside weaker growth helping explain why equity markets have historically fared ever so slightly better during periods of hikes than cuts. It is the conditions, not the policy move, that carry the signal. The same logic applies elsewhere: just as with oil, we cannot predict the path, but we can evaluate how markets have historically responded to the conditions around it, we do not need to forecast Fed decisions to assess the environment they are responding to.