I recently came across an insightful 17-page report on China by Louis-Vincent Gave. Based in Hong Kong, Louis is one of the strategic thinkers I follow closely. My clients are well aware of my long-term view on China and I found Louis’s perspectives particularly relevant to the broader narrative I have been sharing with them over the years.

Here is a section:

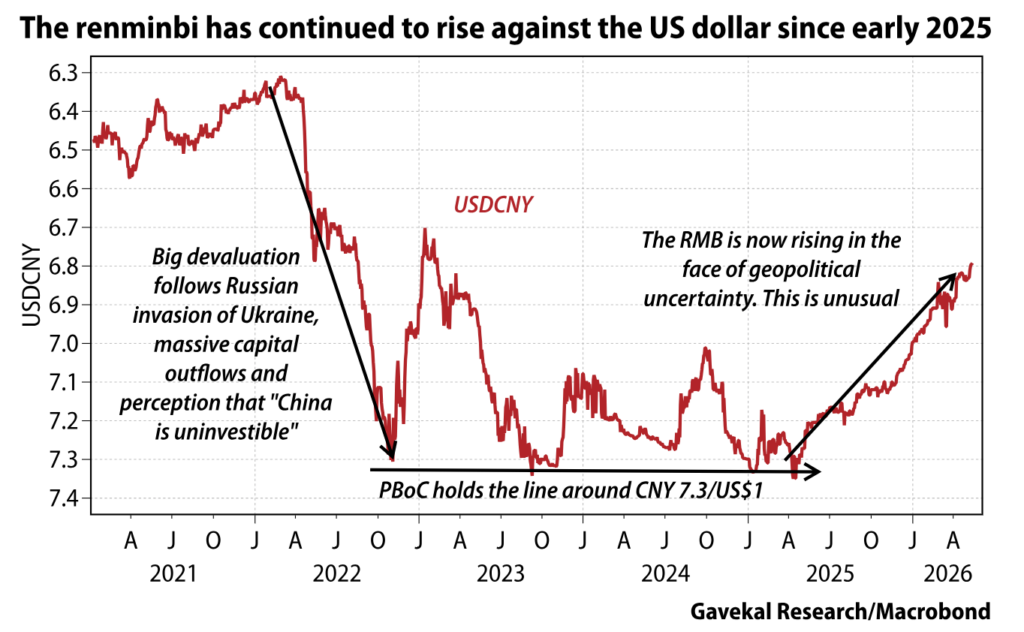

One positive tailwind for both Chinese bonds and equities is the unfolding shift in China’s exchange rate policy. Since early 2025, the renminbi has risen against the US dollar, and most other major currencies, almost every month.

This is an interesting development, especially in the face of the Iran war. In the past, the default mode for renminbi management was to freeze the value of the currency at times of global uncertainty. But not today. Instead, the renminbi continues to grind higher.

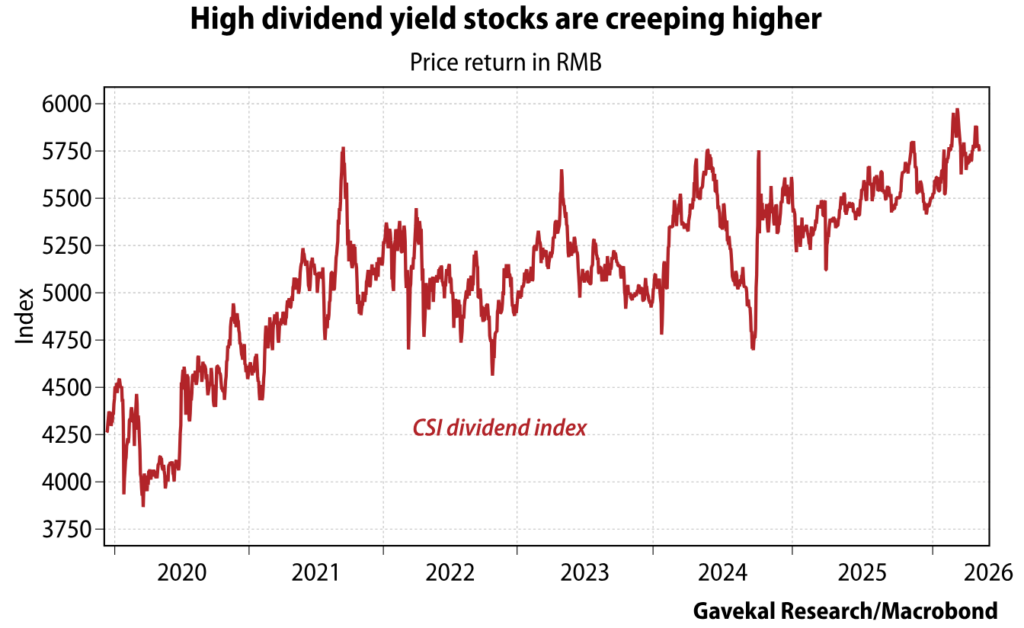

This shift in the renminbi trend, combined with the drop in US short rates, led us to believe that Chinese savings would stop being funneled into US dollar bank deposits, and would instead have no alternative but to look for domestic yield. In reality, this has yet to happen. Sure, high-dividend-yield-paying stocks have continued to do well, but they have not done so at an accelerating pace.

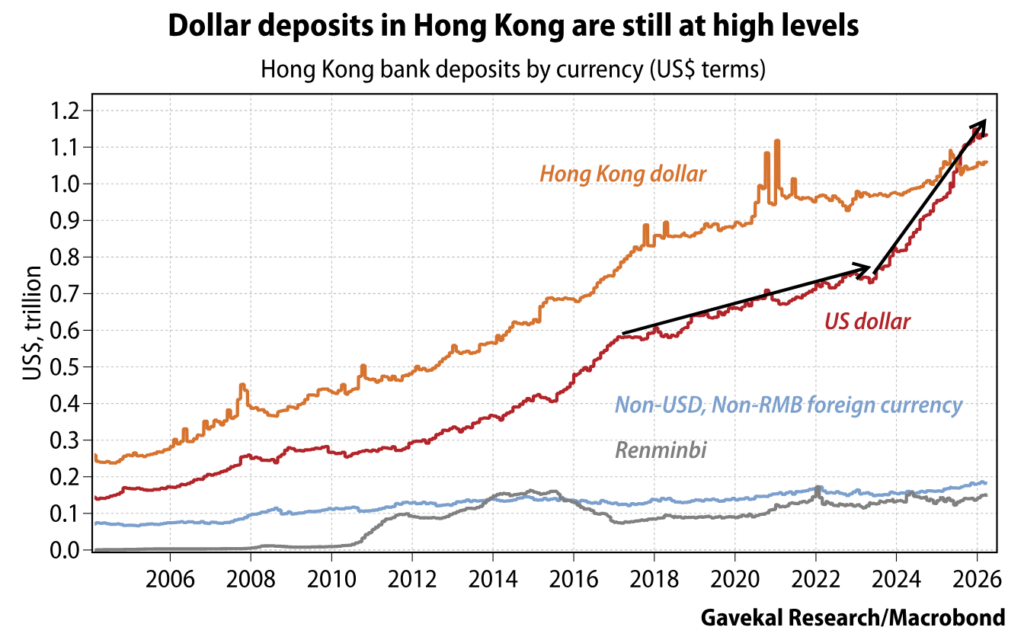

For now, it seems that Chinese money may have stopped flowing into US dollar deposits. At the same time, money previously deployed in US dollars has yet to leave. At least, that is what US dollar bank deposits in Hong Kong would seem to indicate.

Here is his concluding section:

In conclusion, the Chinese equity landscape is constantly evolving. And as things stand, the market continues to offer a number of attractive opportunities. Momentum investors can focus on AI, tech hardware, industrials and materials. Carry investors can look to high-dividend-yielding stocks and banks. Meanwhile, mean-reversion investors may find value in internet names, real estate stocks and consumer names.