I’m not the most active person on LinkedIn, more of a quiet observer who scrolls now and then. I do make new connections occasionally (selectively, of course). At the risk of upsetting some people, LinkedIn can sometimes feel like a stage where many are more interested in “showing off” than sharing real insights or adding value.

One person I always make a point to follow is Denise Chisholm. Her insights are consistently outstanding, often making me pause, think, and challenge my own views. Here is another timely piece from her.

Here is a section:

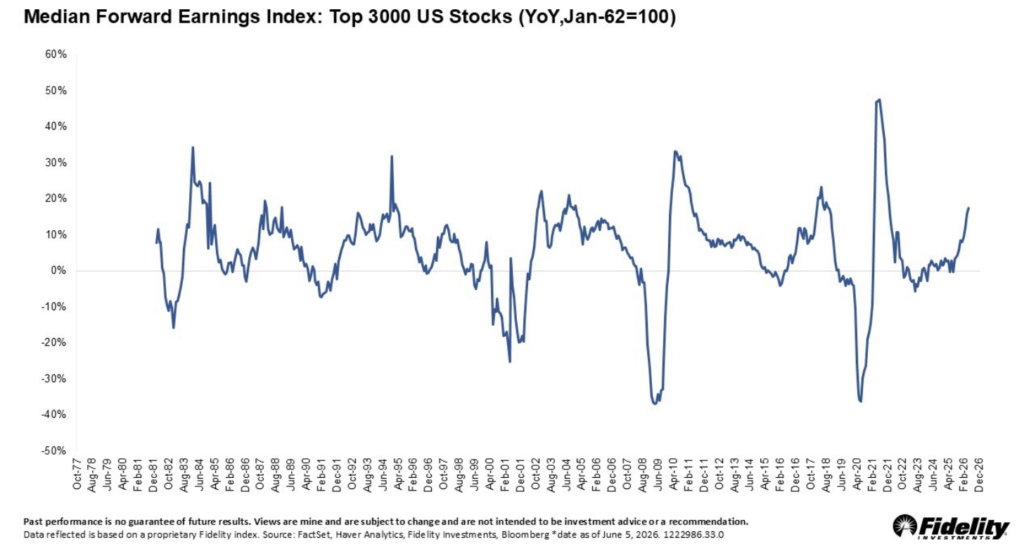

Earnings have quietly become the story again and quickly. Expectations have moved meaningfully higher, with even the median S&P 500 stock now projected to deliver solid double‑digit growth this year according to IBES. That is a sharp shift from where we started, and it comes as we are lapping a period of tariff-related uncertainty that temporarily depressed estimates.

The natural question is whether this kind of strength is something to lean into or something to fade. History, at least on a one-year horizon, does not give much support to the “too good” narrative.

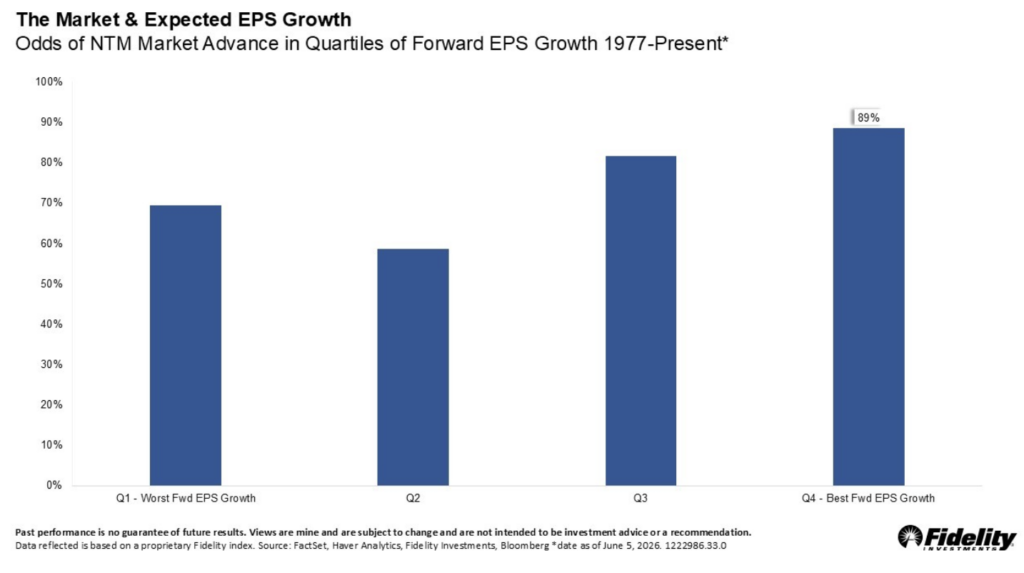

Historically, when you bucket forward earnings growth into quartiles, the odds of market gains have not varied all that much and if anything, environments with strong growth have tended to coincide with better outcomes, not worse. Earnings may lead prices, but the relationship is not one-directional; there are plenty of periods where prices have moved first and fundamentals followed.

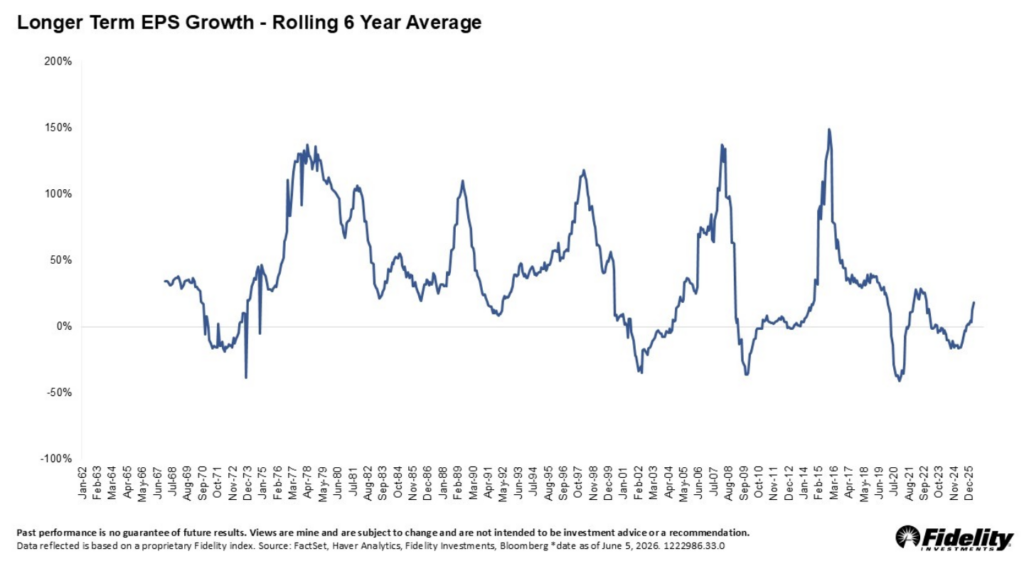

The longer-term view tells a different story and it is the one that helps anchor today’s surge in perspective. When earnings growth has been strong for an extended period, it has typically coincided with the later stages of the economic cycle – periods where growth is robust, sentiment is elevated, and the backdrop starts to look more boom-like. That is why, historically, higher levels of longer-term earnings growth have been associated with lower forward return potential.