Since the April lows, Wall Street’s bull streak has practically defied gravity. Despite a laundry list of worries, stocks have kept charging higher. The S&P 500 has now achieved its third-longest streak of 3‑year highs since 1928, a feat that is as impressive as it is puzzling. This relentless rally has been fueled by a potent cocktail of AI euphoria, abundant liquidity, and retail buying, seemingly unfazed by the occasional market warning sign.

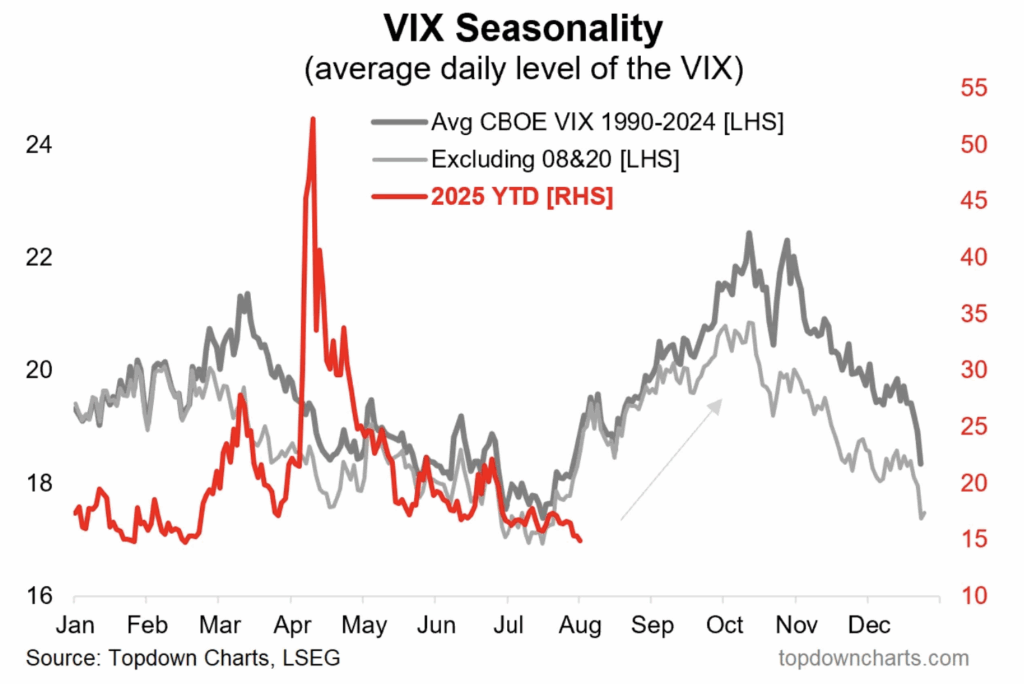

Well, now comes August and September, historically the market’s “grumpy months” and this is when volatility tends to creep back into the spotlight. Several factors make this period seasonally weak. Earnings season winds down, trading volumes thin out as Wall Street decamps to the Hamptons and low liquidity often exaggerates market mood swings.

The timing is delicate, as the recent weak payrolls report has shifted the Federal Reserve’s focus toward slowing economic growth, and market sentiment is now leaning heavily toward a September rate cut with Fed funds futures pricing in an 87% probability. Actually, the employment data is not as bad as some are making it out to be.

History shows that 5-10% corrections during these months are as common as pumpkin spice lattes in the fall even in the middle of strong bull markets. For some investors, this is a good time to move from an “all gas, no brakes” mindset to something more balanced.

The broader bull market still looks alive and well heading into year‑end, but the path over the next couple of months could feel more like a rollercoaster than a smooth climb. Our approach focuses on maintaining balance, selectively adding where conviction is highest, and letting our alternative strategy do the heavy lifting.